Using Your Tax Refund To Achieve Your Homeownership Goals This Year

If you’re buying or selling a home this year, you’re likely saving up for a variety of expenses. For buyers, that might include things like your down payment and closing costs. And for sellers, you’re probably working on a bit of spring cleaning and maintenance to spruce up your house before you list it.

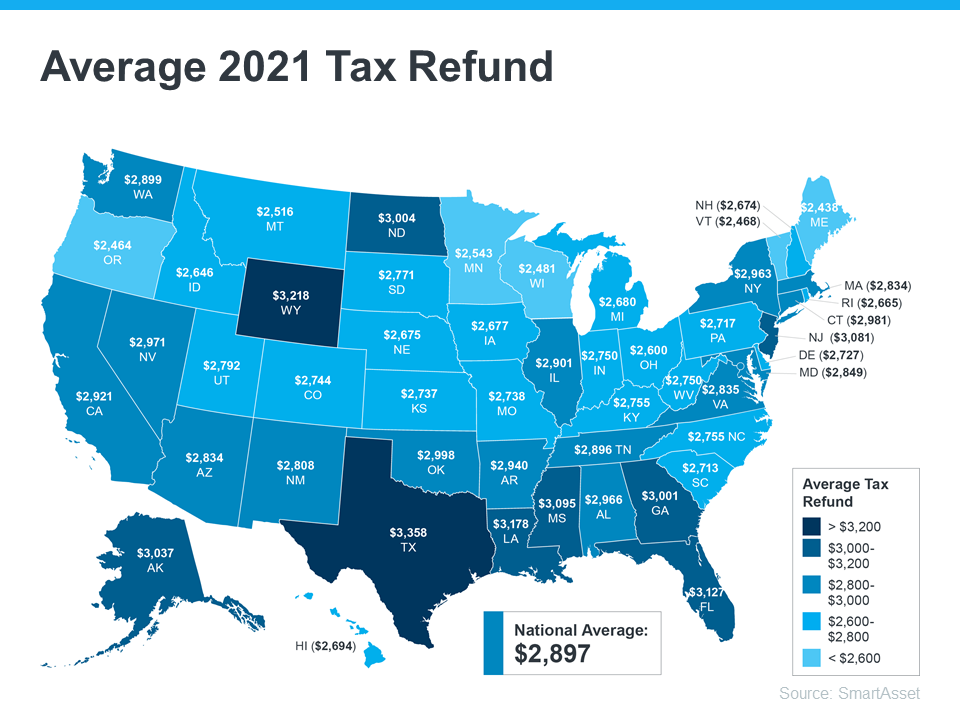

Either way, any money you get back from your taxes can help you achieve your goals. Using a tax refund is a common tactic for buyers and sellers. SmartAsset estimates the average American will receive a $2,897 tax refund this year. The map below provides a more detailed estimate by state:

If you’re getting a refund this year, here are a few tips to help with your home purchase or sale this season.

How Buyers Can Use Their Tax Refund

According to American Financing, there are multiple ways your refund check can help you as a homebuyer. A few include:

Growing your down payment fund – If you haven’t started saving for your down payment, let your tax refund kick off the process. And if you have a fund already, the money you get back could put you closer to your goal.

Paying for your home inspection – Your home inspection can save you a lot of headaches down the road by helping you determine the condition of the house. As a buyer, you’ll typically be responsible for paying for your inspection, and it’s definitely worth the investment.

Saving for closing costs – Closing costs are additional expenses you’ll need to pay once it’s time to close. They average anywhere between 2-5% of the purchase price of your home.

This list is a great start, but it isn’t exhaustive of all the costs you may encounter as you set out on your homebuying journey. The best way to prepare is to work with a trusted real estate professional to make sure you understand what’s to come in the process.

How Sellers Can Use Their Tax Refund

If you own a home and are planning to sell this spring, your tax refund can help you make sure your home is ready to list. Here are a few ways current homeowners can put their tax refund to good use:

Making small upgrades – NerdWallet provides a list of great ways to use your tax refund, including tackling small projects or boosting your curb appeal to help your home stand out.

Making repairs – If there’s anything in your house that needs to be fixed, American Financing notes that completing repairs is another great use of that money.

Buying your next home – Whether you’re selling to move up or downsize, you can use your tax refund to help pay for any costs on the purchase of your next home.

Of course, it’s important to talk with your trusted real estate advisor before taking on any projects. They’ll make sure you can focus on areas that’ll help you receive the best possible price when you sell.

Bottom Line

Funding your home purchase or sale can feel like a daunting task, but it doesn’t have to be. Your tax refund can help you reach your goals. Let’s connect to discuss how you can start on your journey.

The Best Week To List Your House Is Just Around the Corner

Are you thinking about selling your house? If so, you may want to make it a priority to start the process soon. According to realtor.com, the sweet spot for sellers is just around the corner. In a recent study, experts analyzed housing market trends by looking at data from the past several years (excluding 2020, since it was an atypical year). When applied to the current market, experts determined the ideal week to list a house this year. The research says:

“Home sellers on the fence waiting for that perfect moment to sell should start preparations, because the best time to list a home in 2022 is approaching quickly. The week of April 10-16 is expected to have the ideal balance of housing market conditions that favor home sellers, more so than any other week in the year.”

If you’ve been putting your move on the back burner waiting for the ideal time to sell, you should know your golden window of opportunity is coming up. If you’re able to get your house ready quickly, here’s what you can expect from that week.

You Should See More Buyer Activity

The article expects higher buyer demand based on what’s happened in previous years. This could result in increased competition among buyers and ultimately a bidding war over your house. And since mortgage rates recently ticked up over 4%, chances are good that analysis is right. When rates rise, experts say buyers often hurry to make their purchase before rates climb higher. As Nadia Evangelou, Senior Economist and Director of Forecasting at the National Association of Realtors (NAR), says:

“. . . Buyers are rushing to lock in lower rates as the outlook is for even higher mortgage rates in the following months.”

Your House Is Expected To Sell Quickly

Additionally, the realtor.com analysis shows houses sell even faster during this week of the year, likely due to the heightened buyer demand. If you work with a trusted real estate professional to price your house right, it should sell quickly. And when homes are already selling in just 18 days according to NAR, that could set you up for a big win.

Your House Will Be in the Spotlight

Since the beginning of the year, the number of homes available for sale has been at or near record lows. According to the realtor.com study, the typical trend for this week of the year is that there will be even fewer sellers on the market. If you list when inventory is low, your house will be the center of attention for eager buyers craving options.

If you’re ready to move fast, you may want to shoot for April 10th-16th as your target goal. Just remember, even if you’re not ready to list within the next couple of weeks, rest assured this is still a hot sellers’ market. If you list later in April, you’ll still be in the driver’s seat.

Bottom Line

Ready to get the ball rolling? Let’s connect and schedule a time to go over your next steps. In the meantime, make a checklist of things you need to tackle to get your house ready. When we talk, we can prioritize your to-do list and get you on the road to selling your house.

4 Simple Graphs Showing Why This Is Not a Housing Bubble

A recent survey revealed that many consumers believe there’s a housing bubble beginning to form. That feeling is understandable, as year-over-year home price appreciation is still in the double digits. However, this market is very different than it was during the housing crash 15 years ago. Here are four key reasons why today is nothing like the last time.

1. Houses Are Not Unaffordable Like They Were During the Housing Boom

The affordability formula has three components: the price of the home, wages earned by the purchaser, and the mortgage rate available at the time. Conventional lending standards say a purchaser should not spend more than 28% of their gross income on their mortgage payment.

Fifteen years ago, prices were high, wages were low, and mortgage rates were over 6%. Today, prices are still high. Wages, however, have increased, and the mortgage rate, even after the recent spike, is still well below 6%. That means the average purchaser today pays less of their monthly income toward their mortgage payment than they did back then.

In the latest Affordability Report by ATTOM Data, Chief Product Officer Todd Teta addresses that exact point:

“The average wage earner can still afford the typical home across the U.S., but the financial comfort zone continues shrinking as home prices keep soaring and mortgage rates tick upward.”

Affordability isn’t as strong as it was last year, but it’s much better than it was during the boom. Here’s a chart showing that difference:

If costs were so prohibitive, how did so many homes sell during the housing boom?

2. Mortgage Standards Were Much More Relaxed During the Boom

During the housing bubble, it was much easier to get a mortgage than it is today. As an example, let’s review the number of mortgages granted to purchasers with credit scores under 620. According to credit.org, a credit score between 550-619 is considered poor. In defining those with a score below 620, they explain:

“Credit agencies consider consumers with credit delinquencies, account rejections, and little credit history as subprime borrowers due to their high credit risk.”

Buyers can still qualify for a mortgage with a credit score that low, but they’re considered riskier borrowers. Here’s a graph showing the mortgage volume issued to purchasers with a credit score less than 620 during the housing boom, and the subsequent volume in the 14 years since.

Mortgage standards are nothing like they were the last time. Purchasers that acquired a mortgage over the last decade are much more qualified. Let’s take a look at what that means going forward.

3. The Foreclosure Situation Is Nothing Like It Was During the Crash

The most obvious difference is the number of homeowners that were facing foreclosure after the housing bubble burst. The Federal Reserve issues a report showing the number of consumers with a new foreclosure notice. Here are the numbers during the crash compared to today:

There’s no doubt the 2020 and 2021 numbers are impacted by the forbearance program, which was created to help homeowners facing uncertainty during the pandemic. However, there are fewer than 800,000 homeowners left in the program today, and most of those will be able to work out a repayment plan with their banks.

Rick Sharga, Executive Vice President of RealtyTrac, explains:

“The fact that foreclosure starts declined despite hundreds of thousands of borrowers exiting the CARES Act mortgage forbearance program over the last few months is very encouraging. It suggests that the ‘forbearance equals foreclosure’ narrative was incorrect.”

Why are there so few foreclosures now? Today, homeowners are equity rich, not tapped out.

In the run-up to the housing bubble, some homeowners were using their homes as personal ATM machines. Many immediately withdrew their equity once it built up. When home values began to fall, some homeowners found themselves in a negative equity situation where the amount they owed on their mortgage was greater than the value of their home. Some of those households decided to walk away from their homes, and that led to a rash of distressed property listings (foreclosures and short sales), which sold at huge discounts, thus lowering the value of other homes in the area.

Homeowners, however, have learned their lessons. Prices have risen nicely over the last few years, leading to over 40% of homes in the country having more than 50% equity. But owners have not been tapping into it like the last time, as evidenced by the fact that national tappable equity has increased to a record $9.9 trillion. With the average home equity now standing at $300,000, what happened last time won’t happen today.

As the latest Homeowner Equity Insights report from CoreLogic explains:

“Not only have equity gains helped homeowners more seamlessly transition out of forbearance and avoid a distressed sale, but they’ve also enabled many to continue building their wealth.”

There will be nowhere near the same number of foreclosures as we saw during the crash. So, what does that mean for the housing market?

4. We Don’t Have a Surplus of Homes on the Market – We Have a Shortage

The supply of inventory needed to sustain a normal real estate market is approximately six months. Anything more than that is an overabundance and will causes prices to depreciate. Anything less than that is a shortage and will lead to continued price appreciation. As the next graph shows, there were too many homes for sale from 2007 to 2010 (many of which were short sales and foreclosures), and that caused prices to tumble. Today, there’s a shortage of inventory, which is causing the acceleration in home values to continue.

Inventory is nothing like the last time. Prices are rising because there’s a healthy demand for homeownership at the same time there’s a shortage of homes for sale.

Bottom Line

If you’re worried that we’re making the same mistakes that led to the housing crash, the graphs above show data and insights to help alleviate your concerns.

Real Estate Voted the Best Investment Eight Years in a Row

In an annual Gallup poll, Americans chose real estate as the best long-term investment. And it’s not the first time it’s topped the list, either. Real estate has been on a winning streak for the past eight years, consistently gaining traction as the best long-term investment (see graph below):

If you’re thinking about purchasing a home this year, this poll should reassure you. Even when inflation is rising like it is today, Americans agree an investment like real estate truly shines.

Why Is Real Estate a Great Investment During Times of High Inflation?

With inflation reaching its highest level in 40 years, it’s more important than ever to understand the financial benefits of homeownership. Rising inflation means prices are increasing across the board. That includes goods, services, housing costs, and more. But when you purchase your home, you lock in your monthly housing payments, effectively shielding yourself from increasing housing payments. James Royal, Senior Wealth Management Reporter at Bankrate, explains it like this:

“A fixed-rate mortgage allows you to maintain the biggest portion of housing expenses at the same payment. Sure, property taxes will rise and other expenses may creep up, but your monthly housing payment remains the same.”

If you’re a renter, you don’t have that same benefit, and you aren’t protected from increases in your housing costs, especially rising rents.

History Shows During Inflationary Periods, Home Prices Rise as Well

As a homeowner, your house is an asset that typically increases in value over time, even during inflation. That‘s because, as prices rise, the value of your home does, too. And that makes buying a home a great hedge during periods of high inflation. Natalie Campisi, Advisor Staff for Forbes, notes:

“Tangible assets like real estate get more valuable over time, which makes buying a home a good way to spend your money during inflationary times.”

Bottom Line

Housing truly is a strong investment, especially when inflation is high. When you lock in a mortgage payment, you’re shielded from housing cost increases, and you own an asset that typically gains value with time. If you want to better understand how buying a home could be a great investment for you, let’s connect today.

A Happy Tail: Pets and the Home buying Process

It’s no secret that we love our furry friends – about 70% of U.S. households have pets. What may come as a surprise is how large a role they play in the homebuying process.

Americans spend $1,163 a year on their pets, and nearly half of pet owners say they would move for better accommodations and amenities for their pets.

If you’re thinking of adding a furry friend, or if you already have, let’s connect to discuss how you can find a home that meets all your pet’s needs.